Q3 2024 Quarterly Update

Key Market Insights

- Monetary policy goals have changed from primarily controlling inflation to promoting economic growth. This shift has created a wider range of leadership in financial markets and opened up new opportunities across different sectors and asset classes.

- This change in monetary policy has led to increased market volatility as investors adapt their strategies and close out positions that were previously profitable.

- Market breadth is improving, indicating a healthier and more diverse market environment, which is particularly beneficial to the diverse equity exposure within the T. Bailey funds.

- Ongoing global conflicts remain a source of concern for financial markets, posing a dual threat as a potential source of market volatility and a risk to the current benign inflation.

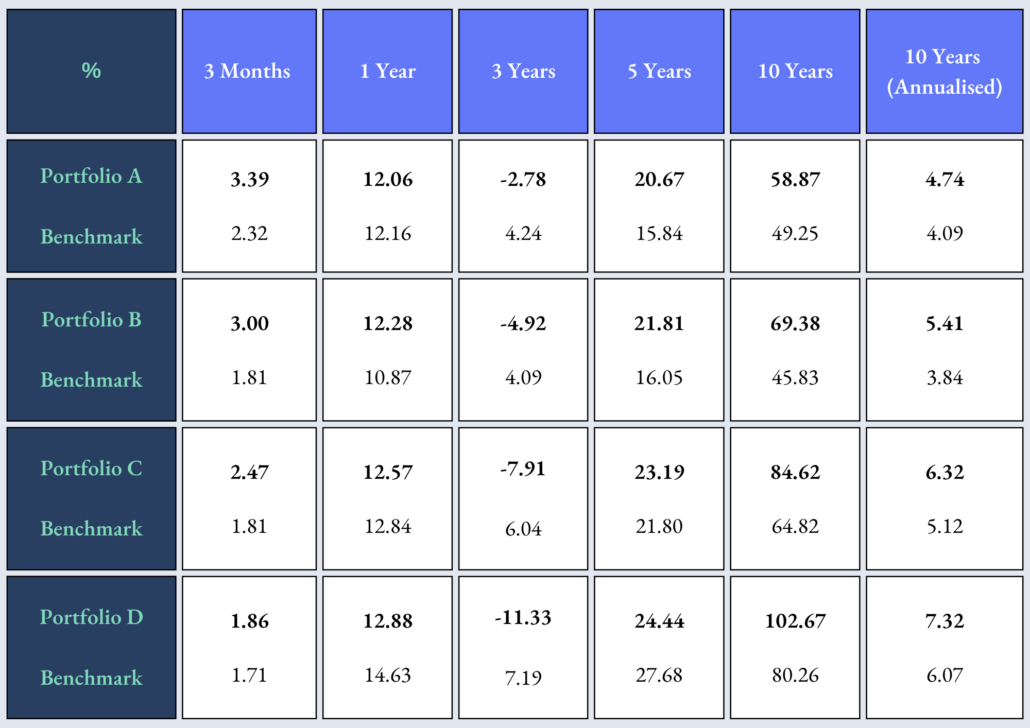

Performance to 30/09/2024 is shown as the total return after investment fees. Past performance is not a reliable indicator of future returns. Capital is at risk. Relevant benchmarks: A (IA Mixed Investment 20–60% Equity) B (ARC Balanced) C (ARC Steady Growth) D (ARC Equity)

Review Of The Markets

The T. Bailey funds experienced modest positive performance in the quarter, masking significant shifts in financial markets. Investors faced conflicting signals as economies continued to cool, leading to a change in central bank priorities after their two-year battle against inflation. The US Federal Reserve initiated an easing cycle by cutting interest rates, following the lead of their European counterparts, including the UK. This shift was driven by their mandate for growth, not just price stability. A notable consequence of these changes was a shift in market leadership, with healthcare, financial, and industrial sectors gaining momentum while the technology sector’s dominance in equity market performance of recent years waned. With UK interest rates expected to remain higher than those in the US, Sterling strengthened. This led to disappointing performance of US equities for UK-based investors when measured in Sterling terms while domestic equities and Asian markets outperformed in aggregate. Chinese stocks surged late in the quarter following a government pledge of widespread support to counter slowing economic growth. Japan took a different approach, using rising inflation as an opportunity to hike interest rates. This led to increased borrowing costs that were particularly detrimental to so-called ‘carry trades’ reliant on cheap financing. A considerable strengthening of the Japanese Yen and a brief period of market volatility ensued part way through the quarter. Barring unexpected shocks, cooling inflation is expected to pave the way for continued interest rate cuts. While this may signal the approaching end of the economic cycle, it currently provides support for both stock and bond returns.

Performance Review

The T. Bailey Dynamic Fund was the strongest performer over the quarter with positive returns broadly built across all asset classes with debt, real assets, absolute return funds, gold and most equity fund holdings performing positively. Chrysalis Investments was a standout performer following the announcement of a bid for one of its investee companies.

Early in the quarter, T. Bailey identified that a softening of interest rates would be positive for closed-ended infrastructure funds that had moved to wide valuation discounts as interest rates rose in 2022. As such, they introduced the VT Gravis UK Infrastructure Fund which performed well, although existing infrastructure and property exposure, through Impact Healthcare REIT and Urban Logistics provided even stronger returns. Each of these positions stands to benefit from improving sentiment towards the listed infrastructure sector as it recovers from a low base and, in the meantime, each generates respectable yields.

With a turn in the interest rate cycle, leadership in equity markets shifted over the quarter as value equities began to perform whilst large-cap US technology stocks underperformed. Ranmore Global Equity and WS Havelock Global Select funds, both having a value-conscious approach to investment, were relatively new positions before the start of the quarter and were additive to performance.

Improving market breadth was also supportive to the positions held in Polar Capital Healthcare Opportunities and Polar Capital Insurance funds as well as to industrial names within the Schroder Global Energy Transition and Schroder Global Sustainable Food and Water funds held.

Perhaps surprisingly, one of the largest detractors to performance came from exposure to the artificial intelligence theme. Strength in this area in recent quarters has seen a rise in valuations and ever greater expectations for future earnings. This presents a challenge and is creating a lot of volatility in this space. The managers of the Polar Capital Artificial Intelligence Fund have identified that there will be a shift away from the large-cap technology companies that enable AI services and are looking to find those companies able to benefit from putting it to use. T.Bailey retains a balanced exposure to the theme compared to other thematic areas such as insurance, healthcare, cybersecurity and energy transition.

Copper detracted marginally from the funds performance over the quarter, as T. Bailey’s exposure, (held through the WisdomTree Copper ETC) is priced in US dollars which struggled to keep pace with the strength of Sterling. However, this was more than compensated for by the returns from the fund’s allocation to gold.

For a more in-depth look at some of the holdings and contributors and detractors to performance in the funds please click below.

As ever, do get in touch with us if you have any questions.

Go well,

Featherstone